| Balance Sheet After Investing | ||||||

| Assets | GB ‘000,000 | Calculations | ||||

| Net Fixed Assets | 70 | Cash&Current Assets | GB’000,000 | |||

| Cash &Current Assets | 16.08 | ROA | 0.15*70 | 10.5 | ||

| Total Assets | 86.08 | ROI | 0.2*30 | 6 | ||

| Less 7% Interest of 6% | -0.42 | |||||

| Financed by | Less Redeemed Debentures | -30 | ||||

| 7% Debentures | 0 | Add Original Cash & C.Assets | 30 | |||

| Equity Capital | 76.08 | 16.08 | ||||

| Current Liabilities | 10 | Debentures | ||||

| Total Capital | 86.08 | Original | 30 | |||

| Less Amount to be redeemed | -30 | |||||

| 0 | ||||||

| Equity Capital | ||||||

| Original E.Capital | 60 | |||||

| Add Retained Earnings | 16.08 | |||||

| 76.08 |

From the above balance sheet, we can see that the firm has the potential to reduce its total amount owed to its investors by paying off their redeemable debentures. To make the deal sweeter, the firm has the ability to increase its equity capital from 60 million pounds to 76.08 million pounds.

Assumptions

| Projected Balance Sheet After Investing | ||||||

| Assets | GB ‘000,000 | Calculations | ||||

| Net Fixed Assets | 70 | Cash&Current Assets | GB’000,000 | |||

| Cash &Current Assets | 12.585 | ROA | 0.12*70 | 8.4 | ||

| Total Assets | 82.585 | ROI | 0.15*30 | 4.5 | ||

| Less 7% Interest of 4.5% | -0.315 | |||||

| Financed by | Less Redeemed Debentures | -30 | ||||

| 7% Debentures | 0 | Add Original Cash & C.Assets | 30 | |||

| Equity Capital | 72.585 | 12.585 | ||||

| Current Liabilities | 10 | Debentures | ||||

| Total Capital | 82.585 | Original | 30 | |||

| Less Amount to be redeemed | -30 | |||||

| 0 | ||||||

| Equity Capital | ||||||

| Original E.Capital | 60 | |||||

| Add Retained Earnings | 12.585 | |||||

| 72.585 |

Task 2

Principle of Contract Costing

Contracts are essentially an agreement between a contractee and a contractor to undertake a certain specific task for a consideration within a specified time period and terms. Contracts have commencement dates and completion dates which are useful in the calculation of costs and amount owed to the contractor, or the reverse if there is a breach of contract. In contract costing, it is important to note that direct costs form bulk of the costs. Contracts are costed depending on the kind of contract they are. We have the following types of contracts. First, Fixed price contracts where a price for the contract is agreed upon by both parties before commencement of the contract. Second, the fixed price contract which has a clause for price change. Third, the cost plus contract where profits for the contractor are determined as a percentage of the costs incurred.

To properly account for costs and revenues for a given contract, two methods can be adopted. First, the architect’s/engineer’s certificate method or two, the work in progress method. With the architect’s certificate method, costs are broken down into direct expenses, indirect expenses, overheads and costs of extra work. Using the above mentioned expense heads, an engineer or an architect can authoritatively give the value of work certified and the value of work not certified. The contractor is then paid for the work certified. In this case, work not certified is treated as an expense. Second is the work in progress method. This method allows the contractor to be paid depending on the percentage of the work completed. Work in progress in this method is assumed to be the work not certified.

Attributable Profits

Attributable Profit =Contract Price-Costs Incurred

Calculation of Costs Incurred

Therefore, Attributable Profit will be calculated as follows.

= (3,500,000)/3-279,700

= 1,166,667-279,700

= 886,967

Value of Work Certified

Value of Work Certified=Total Costs Incurred- Work Not yet Certified

= 279,700-27,000

=257,700

Contract Cost Statement

Mega Construction Plc

Contract Cost Statement

Submitted by,

Name

Position

Contact

For Contract Number XXXX,

Contract Period Covered, 1 March 2011 to 28 February 2012.

On this day 30 of September 2017.

The Contract

This contract was entered into by Mega Construction Plc (contractor) and XXX (contractee). The contract value is 3,500,000 British Pounds. The contract commenced 1 March 2011 and will come to a halt on 28 February 2014 unless otherwise agreed.

Pricing Methods

In line with Regulation 22(2) (K), this contract adopted a fixed pricing method. The contract cost were determined, agreed upon and set at 3,500,000 British Pounds.

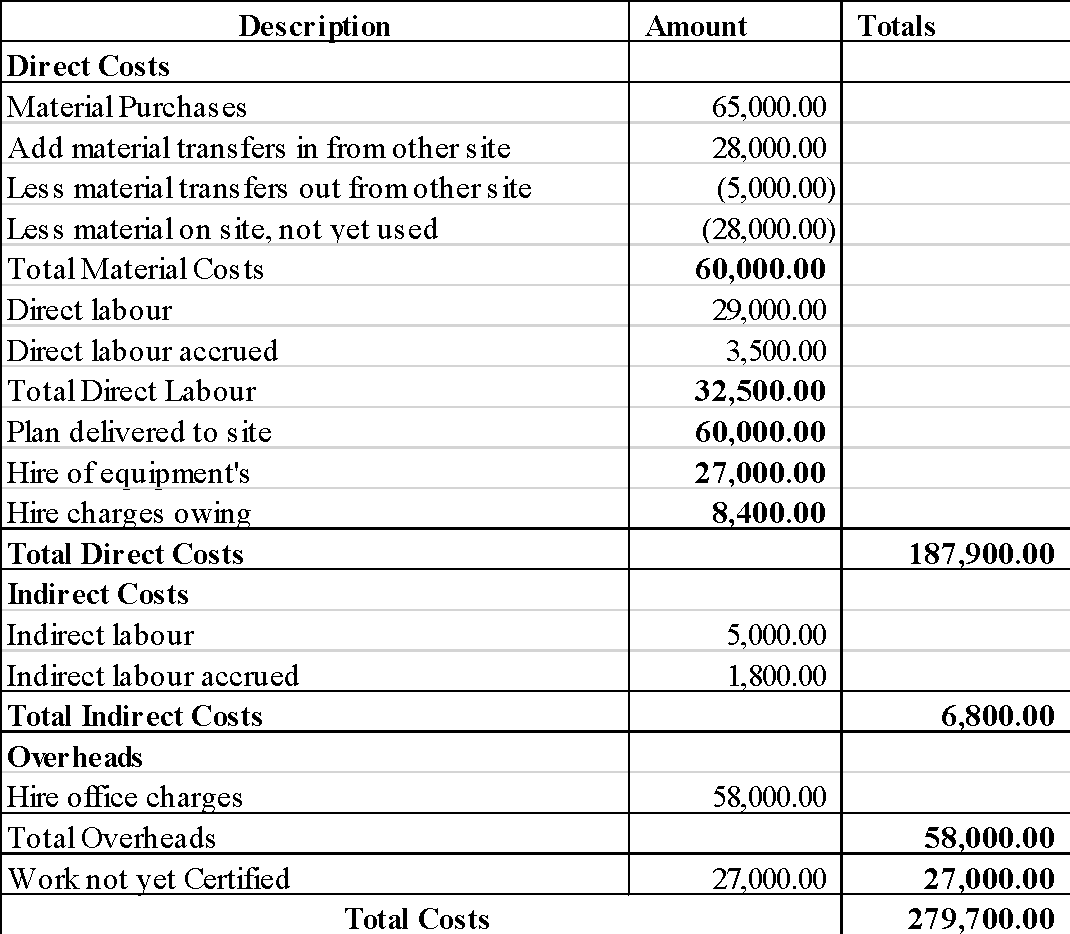

Annual Profile of Costs

Below is a table showing how Mega Construction Plc categorized costs and the specific amounts that matched each expenditure head.

Delivering a high-quality product at a reasonable price is not enough anymore.

That’s why we have developed 5 beneficial guarantees that will make your experience with our service enjoyable, easy, and safe.

You have to be 100% sure of the quality of your product to give a money-back guarantee. This describes us perfectly. Make sure that this guarantee is totally transparent.

Read moreEach paper is composed from scratch, according to your instructions. It is then checked by our plagiarism-detection software. There is no gap where plagiarism could squeeze in.

Read moreThanks to our free revisions, there is no way for you to be unsatisfied. We will work on your paper until you are completely happy with the result.

Read moreYour email is safe, as we store it according to international data protection rules. Your bank details are secure, as we use only reliable payment systems.

Read moreBy sending us your money, you buy the service we provide. Check out our terms and conditions if you prefer business talks to be laid out in official language.

Read more